IFRS 16 - Leasing

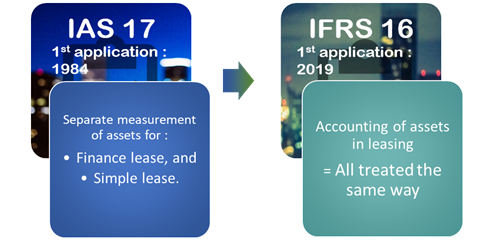

Hardly within a year, international standards on leasing will evolve. Indeed,IFRS 16replaces the standardIAS 17on January 1st, 2019.

Leasing is an important and flexible measure of financing. The new standard will improve the transparency and comparability of information on off-balance sheet leases by bringing them onto the balance sheet.

Core principle of the change in accounting standards about leasing :

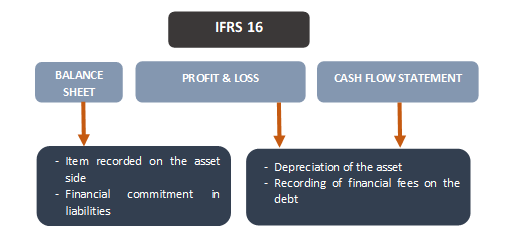

Modifications in financial statements due to implementation of IFRS 16 :

Initially, liabilities are measured at the present value of lease payments that are not paid at that date. Assets, called "right-of-use assets, should be measured at cost (initial measurement of lease liability + any lease payments made at or before the commencement date less any lease incentives received + any initial direct costs incurred by the lessee + an estimate of costs to be incurred by the lessee in dismantling and removing the underlying asset). IFRS 16 demands that banks present lease assets arising from leases of properties as tangible assets. The depreciation of the lease asset and the interest on the liability is recognized in the P&L over the lease term. On this subject, this is similar to the treatment of finance lease under IAS 17, which leads to higher expenses at the start of the term of the lease.

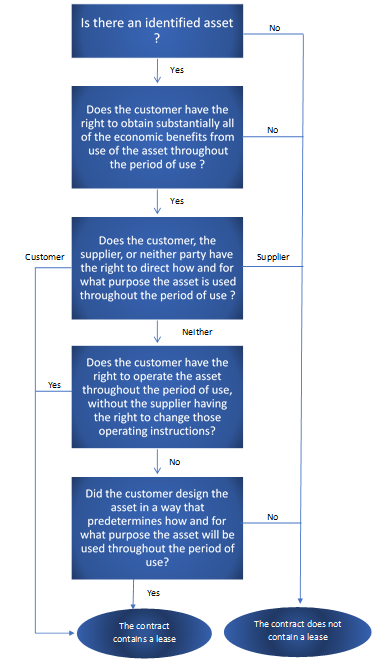

Chart to assess whether a contract contains a lease under IFRS 16 :

What is at stake is the distinction between leases and service contracts.

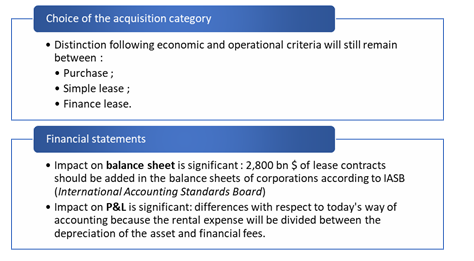

Impacts :

Under IFRS 16, financial institutions with material off-balance sheet "operating leases will report higher assets.

Some assets will not be impacted by this new standard. Assets leased for a short term of less than a fiscal year and the leases of low-value assets will not have to be recognized in the balance sheets of financial institutions. Since the standards do not specify the concept of "low-value, judgement will be necessary.